")

In its Progress Report 2025, Starlink states that: “In 2025, around 6,500 commercial aircraft were equipped with Starlink.” The figure seemingly underscores the rapid momentum the satellite operator has achieved in the in-flight connectivity (IFC) market and reflects the growing appetite among airlines for low-latency, high-throughput broadband. Within the aviation connectivity industry, however, the figure was met with a degree of scepticism and has prompted some discussion about how exactly Starlink arrived at this number.

The statement not only indicates that Starlink has been installed on around 6,500 commercial aircraft, but appears to suggest these installations occurred during 2025 alone. This would imply an even larger cumulative fleet when accounting for aircraft that were already equipped during 2024.

Our analysis at Valour Consultancy suggests the installed base may be significantly smaller depending on how the metric is defined. According to Valour’s IFEC Market Tracker, the number of commercial aircraft actively using Starlink connectivity at the end of 2025 stood at approximately 742 aircraft globally. This difference does not necessarily indicate an error in reporting, but rather highlights the possibility that the two figures are measuring slightly different things.

One plausible explanation is that Starlink’s figure refers to the number of installation kits delivered or allocated to airline programmes rather than aircraft already operating with the service. In contrast, Valour’s IFEC Market Tracker defines “installed” as aircraft actively connected to and operating on the service provider’s network.

Installation timelines in aviation connectivity programmes can be lengthy, even after agreements are announced and hardware is delivered. Aircraft must be taken out of service for modification, installation slots must be scheduled within airline maintenance cycles, and certification requirements must be met. As a result, there can be a considerable lag between a connectivity contract being announced and aircraft actually entering service with the system installed.

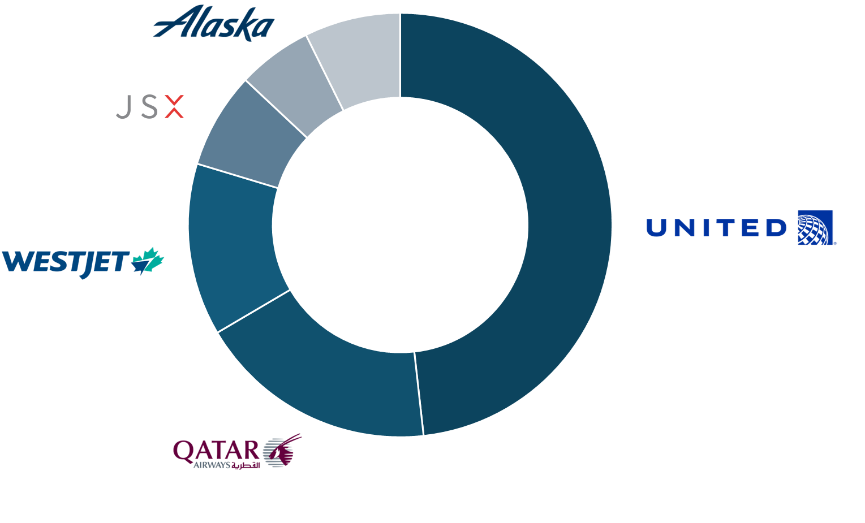

Publicly available airline disclosures illustrate this dynamic. United Airlines confirmed it had 300 Starlink-connected aircraft in February 2026, making it by far the largest deployed fleet. Qatar Airways has also made significant progress in its installation programme; while rollouts on Air France, Alaska Airlines, and WestJet are also well under way. Beyond that, however, many of the other large-scale Starlink programmes had not yet progressed to installation.

Starlink’s Largest Active Commercial Fleets by Airline

Source: Valour Consultancy ’s IFEC Market Tracker

Even when an airline wants to move quickly, certification, supply chain logistics, and operational planning can slow the pace of installations. The experience of ZIPAIR Tokyo offers a good example. The carrier first announced it had selected Starlink in 2023, but its first aircraft was only connected in February 2026, illustrating the extended timeline that can accompany even relatively small fleet deployments.

None of this diminishes the broader impact Starlink is already having on the IFC market. At Valour Consultancy, we estimate the satellite operator now has contracts covering around 8,000 commercial aircraft globally. As these programmes mature and installations accelerate, the number of aircraft actively connected to the Starlink network is expected to rise rapidly over the coming years. Valour Consultancy’s report on The Future of In-Flight Connectivity dives into this pressing issue, mapping out what the next decade holds and providing forecasts with robust justifications.