The proposed €1.2 billion acquisition of IDEMIA’s Public Security (IPS) division by Amadeus IT Group marks a significant step in the continued convergence of travel technology and government border infrastructure. It is also one of the most consequential developments in the evolution of the airport and border technology ecosystem in recent years, following several other notable acquisitions in the past two years.

At a high level, the rationale is clear. Amadeus is accelerating its push beyond traditional airline IT, passenger facilitation for airports, and hospitality into a broader, more integrated position across the travel and border ecosystem. Following its previous acquisition of Vision-Box, this deal significantly strengthens its position in biometrics and border management, positioning the company as a credible end-to-end partner for governments.

At the same time, the deal raises important questions around valuation, portfolio fit, and how Amadeus will manage a materially broader set of capabilities and customer segments.

Building an End-to-End Border Ecosystem

The combination of Vision-Box and IPS creates a powerful portfolio spanning:

- Biometric capture and identity verification

- Automated border control (ABC) hardware and platforms

- Passenger flow orchestration

- Backend identity management systems

This aligns with a broader industry shift: governments and airport operators increasingly favour integrated platforms over fragmented vendor ecosystems. Amadeus is effectively betting that the future of border control will mirror the evolution of airline IT, i.e. platform-based, data-driven, and increasingly integrated across stakeholders.

The Vision-Box deal was completed in 2024 (covered in our previous article, ‘Rock Me Amadeus’), and my belief is that this move for IPS has been under consideration since early in 2025. From that perspective, the acquisition is less opportunistic and more a continuation of a deliberate strategy to move into government-facing infrastructure.

The Strategic Tension: Core vs Peripheral Markets

Where the deal becomes more complex is in the composition of IPS itself.

Unlike Vision-Box, IPS’s portfolio extends well beyond travel:

- Law enforcement solutions

- Criminal identification systems

- Access control technologies

- Civil identity programmes

These areas sit outside Amadeus’ traditional – and arguably logical – focus on travel-related operations and those adjacent to it (e.g. corporate travel and expenses, hospitality, epayments and invoicing).

It is difficult to see a strong strategic rationale for Amadeus to remain active in law enforcement or broader public security markets; they are not an obvious natural fit for Amadeus. There is plenty of alignment, but does Amadeus want to be issuing driver’s licenses in North America or providing video analytics and fingerprinting capabilities for police departments? These sectors involve different procurement cycles, customer relationships, and regulatory frameworks. Whilst a natural fit for IPS’s primary remit, they are less so for the airline, airport, and border ecosystems that underpin Amadeus’ core business.

This raises a key question: is this acquisition about capability expansion, or portfolio acquisition with an eventual carve-out?

A Break-Up Scenario?

There is a credible argument that IPS is more valuable in parts than as a whole.

Examples of two companies that are more natural homes for the non-travel components are:

- Thales Group – already deeply embedded in government security, biometrics, border management and law enforcement

- ASSA ABLOY (via HID Global) – established positioning in identity, access control, a supplier of components of border control and law enforcement systems and hardware, with an increasing focus on airport solutions

An argument could be made for the splitting IDEMIA’s assets between a travel-focused player (Amadeus, SITA) and a security-focused player (Thales, HID, NEC). Ironically, this alignment was physically illustrated at Passenger Terminal Expo, where IDEMIA sat between HID and Amadeus. This is particularly so given that Advent International has effectively been exploring exit options since IDEMIA’s strategic restructure almost two and a half years ago. The tricky bit would be the dividing of technology that overlaps both parts of the business.

Strategic Positioning: Expansion and Customer Reach, Not Reinvention

Compared to established players such as Thales Group or identity and access control specialists like HID Global (part of ASSA ABLOY), Amadeus is approaching the government and security market from a very different starting point.

For those companies, identity, security and government programmes are core revenue drivers.

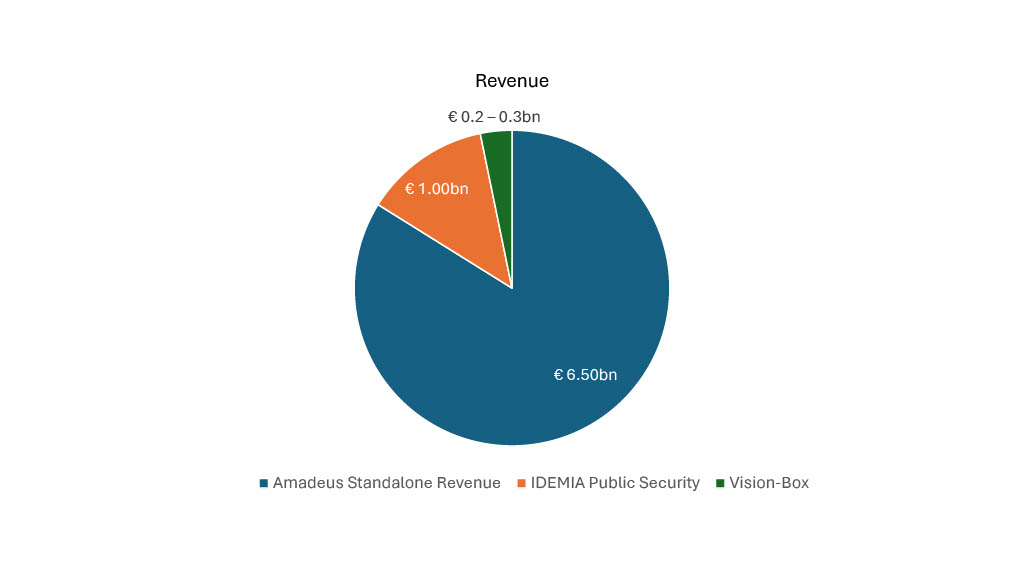

For Amadeus, they remain adjacent extensions of a travel-led model. Based on previously reported figures:

- Amadeus standalone revenue: ~€6.5bn

- IDEMIA Public Security: ~€1.0bn

- Vision-Box: ~€0.2–0.3bn

From a revenue perspective, the acquisition is significant but not transformative in terms of overall mix. With IPS, borders and government jumps from an estimated low single digit percentage of revenue to something more established and prominent, likely accounting for around 15% of annual income. With its high travel (IT)-related revenues, the acquisition does not reposition Amadeus as a government-centric player. Instead, it builds upon its existing operations and establishes a notable, complementary revenue stream that extends its role within the travel ecosystem, plus wider government, law enforcement and access control sectors.

Beyond revenue mix, the acquisition materially expands Amadeus’ capabilities:

- From airport IT into full border management systems

- From passenger processing into national identity infrastructure

- From airline and airport customers into more direct government relationships

It also enhances its position as an end-to-end provider, combining:

- Travel distribution

- Airline and airport IT and passenger facilitation

- Biometric identity and border control

This broader portfolio aligns with a growing market preference for integrated platforms spanning the entire passenger journey, from booking through to border clearance and beyond into hospitality and hotels.

Implications for the Market

If completed, this acquisition significantly reshapes the competitive landscape:

- Amadeus emerges as a top-tier player in border and airport biometrics – and for wider government and (biometric) security solutions

- Traditional airport IT solution providers, such as SITA and Colins Aerospace, will have to reassess their positioning and border control-related strategies

- The market continues to consolidate around fewer, larger platform providers (although there remains plenty of room for specialist airport solution providers to serve local markets and small to medium sized airports)

Perhaps most importantly, it signals a convergence between travel IT and government border infrastructure—a trend that has been building for years but is now accelerating.

What Happens Next?

The key unknowns are not about the acquisition itself, but what follows:

- Will Amadeus retain or divest non-travel and border business lines?

- How will it integrate IDEMIA’s government-led delivery model with its existing business?

- Can it successfully reposition itself as a government partner, rather than a leading travel IT provider?

This deal has been anticipated for some time; in fact, I was asking about it at last year’s Passenger Terminal Expo in Madrid – but this announcement brings these questions into sharper focus. What is clear is that Amadeus is no longer positioning itself solely as a travel technology provider. Instead, it is evolving towards a broader role at the intersection of travel, identity, and border infrastructure, with this acquisition marking a significant step in that direction.

John Devlin, Airports & Borders Director john.devlin@valourconsultancy.com

Are you interested in exploring further insights across the airports and borders sectors? Feel free to email me to organise an introductory call or sign up to our free newsletter here to receive our latest market intelligence updates.

Download our “Biometrics and Digital Identity In Aviation” whitepaper to discover why many biometric programmes are stalling after the trial period, or request a copy of our recent report on ‘The Seamless Passenger Journey in Smart Airports’. This offers an analysis of the competitive landscape across 39 companies, as well as installed base and annual installations for products, along with related touchpoint and service revenues, seamless market value, total market value, biometric attach rates, and the total available market.