The 2025 edition of the Dubai Air Show kicked off with a bang, as Emirates announced a fleetwide contract with Starlink, giving the U.S satellite operator another major customer in the region alongside Qatar Airways. This was immediately followed by news that Starlink had secured a 100+ aircraft deal with flydubai. In this article, Valour Consultancy examines the current state of play in the Middle East, why the region has historically been such a challenge for in-flight connectivity (IFC) vendors, and how Starlink is benefitting by claiming some of the world’s leading airlines.

The Current State of Play

The Middle East represents a golden prize in the IFC market. A regional fleet of over 2,300 commercial aircraft, many of which are operated by prestige airlines that demand best-in-class passenger experiences, highlights why the market is such an attractive proposition.

Just over 1,000 commercial aircraft are equipped with IFC in the Middle East. At 47% of the total regional fleet, this penetration rate is relatively high compared to other parts of the world, but it still leaves a sizable addressable market of unconnected aircraft for vendors to fight over. Moreover, many of those aircraft already connected are ripe for upgrades to low Earth orbit (LEO) or multi-orbit services as airlines in the region look to remain competitive. This means big fleets, big potential, and even bigger budgets – marking the region out as a key battleground for IFC vendors.

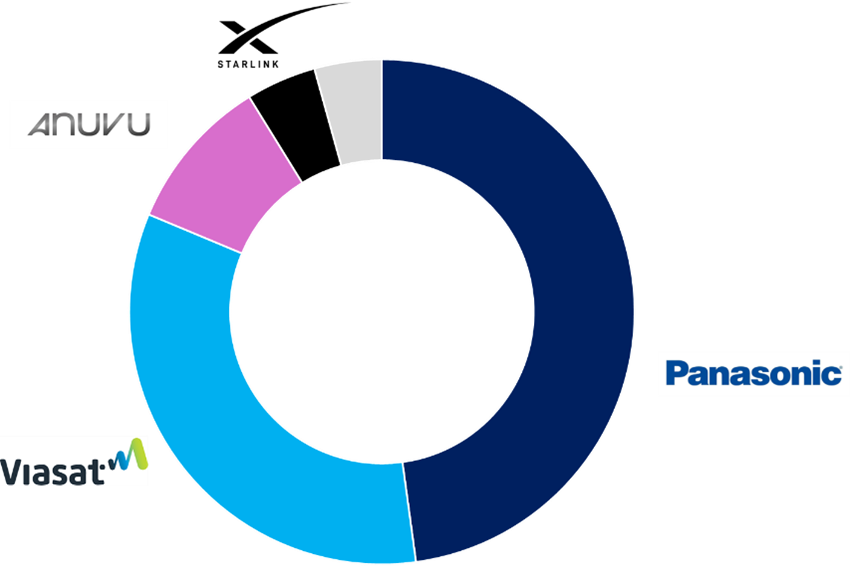

Panasonic Avionics (PAC) is currently the leading IFC service provider in the Middle East, with a 48% share of the active installed base. PAC does not own satellite capacity; instead, it leases capacity from satellite operators and stitches together a network capable of serving airline customers. Its customers include Turkish Airlines, Emirates, and Etihad Airways. Viasat is the other major service provider in the region, with a market share around 33% and its solutions are installed on Emirates, Saudia, and Qatar Airways.

Wins for longstanding vendors in the market are still coming too. The show saw Viasat announce an extension of its deal with Etihad Airways to provide its upcoming AMARA service across the carrier’s fleet, including its new A321LRs. Earlier this year, Royal Jordanian also confirmed plans to roll out Viasat’s Ka-band service on its fleet of more than 40 aircraft.

Despite their current duopoly, PAC and Viasat are not the only show in town. NEO Space Group (NSG), a new commercial space services company backed by Saudi Arabia’s Public Investment Fund (PIF), has already made significant noise. The company has struck deals to provide IFC services to Thai Airways for more than 80 B777s, as well as the airline’s yet-to-be-delivered A321neo aircraft. NSG will also equip Turkish Airlines fleet of 14 A350s, with deliveries beginning in 2026, and more recently announced a deal with Uzbekistan Airlines for the carrier’s incoming A321neos. With substantial financial backing, a flexible solution, and the increasing desire for sovereign space assets, NSG’s is well-positioned to accelerate its expansion across the Middle East and beyond.

IFC Service Provider Market Share in the Middle East (Q2 2025)

Source: Valour Consultancy’s Quarterly IFEC Market Tracker

Beyond satellite connectivity, other options are emerging in the region. Air-to-Ground (ATG) specialist SkyFive has established a presence in Saudia Arabia having signed a MoU with stc Group and Flynas with the aim of providing IFC services across the fleet of one of the region’s largest low-cost carriers (LCCs). The German ATG provider also has an agreement in place with Viasat that will enable aircraft fitted with the latter’s European Aviation Network (EAN) solution to roam into SkyFive’s Saudi ATG network and beyond.

The Middle East Challenge

The Middle East has a higher proportion of aircraft running long-haul routes than is typically found elsewhere. In fact, widebodies account for over 38% of commercial aircraft operating in the region, compared with around 15% in Europe and just 8% in North America. It is the scale of these routes (as well as a comparative lack of dedicated capacity) that has made IFC such a challenge. Larger carriers have typically struggled to find a single solution that can deliver reliable coverage across expansive route networks. As a result of frustration with inconsistent GEO coverage, several major airlines – including Emirates, Qatar Airways, Etihad, and Saudia – have hung onto cheaper but more predictable L-band solutions installed many years ago. The reader may be surprised to learn that even today, more than 200 aircraft in the Middle East still rely on the technology. But with IFC now entering an era of high-speed, low-latency LEO connectivity, narrowband services are no longer viable for leading carriers. Enter Starlink.

Starlink Seizes the Day

Our “Starlink Aviation Deep Dive report” emphasises that Starlink is perfectly positioned to grab a significant chunk of the region thanks to its first to market LEO-only service (beating the likes of Amazon Leo – formerly Kuiper – which won’t be commercially available until at least 2027) and its ability to address capacity and consistency of coverage challenges that have caused performance issues for many deployments in the Middle East. Its unlimited data proposition is expensive, but that matters less in the Middle East than it might elsewhere.

Starlink’s network is already certified for use in Qatar, Bahrain, Jordan, Oman, and Yemen. In May 2025, Starlink was also approved for use in the aviation and maritime sectors in Saudi Arabia. Starlink is still awaiting approval in the UAE and Kuwait.

Starlink, of course, has already secured Qatar Airways, which activated service in October 2024. The carrier has now connected around 100 aircraft, thereby securing the company a foothold in the region.

Rumours had been swirling for a long time that Starlink had won a big contract to serve Emirates and an official announcement was finally confirmed at the opening of the 2025 Dubai Air Show. As per the agreement, “Emirates plans to install Starlink on all its in-service fleet” – a total of 232 aircraft, primarily B777s and A380s. Although not explicitly mentioned, the airline’s 13 active A350s are understood to be included. The first aircraft was equipped and had its debut flight on 23rd November 2025, with the broader deployment set for completion by mid-2027 at a rate of 14 installations per month.

The result of all this is that Starlink now has more than 500 commercial aircraft in the Middle East committed to its service, though only around 100 are currently active. This cements its place as the vendor with the largest backlog – and the largest number of committed aircraft – in the region. So, what next for Starlink? Well, more opportunities exist – notably Singapore Airlines, which is thought to be the next in line following a recent earnings call where the carrier revealed it would install LEO as early as next year. A number of major airlines, including some in the Middle East have yet to make a LEO/multi-orbit play. Given how the market has shaped up over the last 12 months, few would back against Starlink announcing more wins in the near future.