Line fit offerability is key to success in the market for seatback in-flight entertainment (IFE). Almost all wide-body aircraft enter service with a system installed at the factory, while the IFE attach rate in the narrow-body segment stood at 20% in 2022. This is a smidgen higher than the 17% average over the course of the last ten years and proof – were it needed – that there is plenty of life left in the old dog yet (the death knell for seatback IFE has been prematurely sounded too many times to mention).

In contrast, providers of wireless IFE (W-IFE) systems have been much more reliant on the aftermarket to win business. Of the near 9,000 aircraft with such a solution installed at the end of Q1 2023, ~90% were retrofitted into existence. That is, they were installed after the aircraft entered service. And this makes sense given the primary focus for many of these vendors is the single aisle segment, which, in the W-IFE market’s formative years, was home to a huge total addressable market of aircraft without any form of IFE whatsoever. However, there is every indication that line fitments will take on an increasingly important role over the next few years as the W-IFE installed base continues to grow and the remaining pool of aircraft with no IFE shrinks.

One of the main reasons for this is the added flexibility afforded by newer solutions. A case in point is Airbus Airspace Link, which gives airlines the opportunity to specify server units and wireless access points (WAPs) from Airbus subsidiary, KID-Systeme, at the time of the aircraft’s manufacture. In much the same way that the OEM’s HBCplus programme enables airlines to switch bandwidth suppliers without changing the line fit in-flight connectivity (IFC) hardware on their aircraft, clients can somewhat de-risk their investment by choosing software to ride on top of this equipment from one of three different W-IFE providers – Bluebox Aviation Systems, Inflight Dublin and Display Interactive.

Though Airbus Open Software Platform (OSP) – as it was known at the time – formally launched in 2019, deliveries of new aircraft fitted with the system have been slow thanks in the main to pandemic-related uncertainty and budgetary constraints. But with COVID-19 seemingly now in the rear view mirror, activity is once again starting to pick up. Since Titan Airways took delivery of an A321LR configured with Bluebox’s Blueview digital solution, Jetstar and Air Malta have confirmed that they will also offer Blueview on new A320-family aircraft. Inflight Dublin, meanwhile, has stated that Tunisair and another as yet undisclosed customer have ordered Airbus aircraft that will come with the firm’s competing software solution and IFE content.

Another reason is a shift away from more traditional IFE content such as movies, TV shows, music and games towards increased digitalisation of cabin services. As we’ve previously covered, the “E” in IFE is becoming more about engagement for a number of recent airline adopters. easyJet is a notable example and will soon add an order-to-seat capability to its newly fitted infotainment portal, following in the footsteps of fellow AirFi customer, Corendon Dutch Airlines. It stands to reason that providing airlines with the ability to engage and entertain passengers whilst also earning ancillary revenue elevates the overall attractiveness of IFE – especially given the rise of the “bring your own licence” trend that sees many travellers board the aircraft with offline content stored in their streaming platform(s). And in-flight engagement is particularly compelling to the low-cost carrier (LCC) and leisure airline crowd, which, together, account for a substantial number of aircraft on order.

Another reason is a shift away from more traditional IFE content such as movies, TV shows, music and games towards increased digitalisation of cabin services. As we’ve previously covered, the “E” in IFE is becoming more about engagement for a number of recent airline adopters. easyJet is a notable example and will soon add an order-to-seat capability to its newly fitted infotainment portal, following in the footsteps of fellow AirFi customer, Corendon Dutch Airlines. It stands to reason that providing airlines with the ability to engage and entertain passengers whilst also earning ancillary revenue elevates the overall attractiveness of IFE – especially given the rise of the “bring your own licence” trend that sees many travellers board the aircraft with offline content stored in their streaming platform(s). And in-flight engagement is particularly compelling to the low-cost carrier (LCC) and leisure airline crowd, which, together, account for a substantial number of aircraft on order.

While Boeing’s rival W-IFE and digital services platform, Digital Direct, is currently only available via retrofit, our expectation is that it will become a catalogue option in time. To some degree, its future depends on how the airframer’s cabin management system (CMS) strategy develops going forward. Indications are that IFC and W-IFE will shift from a buyer-furnished equipment (BFE) to a supplier-furnished equipment (SFE) model as part of a CMS overhaul that embraces the Internet of Aircraft Things in much the same way as the new Airbus Intelligent Core Management Platform (iCMP) does. Should this happen, Immfly, which helped develop the Digital Direct solution, will presumably be in pole position to win any new line fit W-IFE business that comes Boeing’s way.

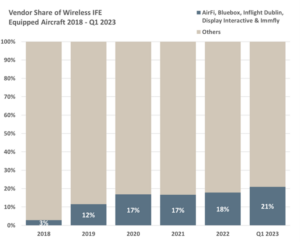

As such, it seems likely that the companies mentioned in this article will be in a strong position to pull away from the more than 30 vendors currently active in the W-IFE market in the coming years. Indeed, the combined market share of Bluebox Aviation Systems, Inflight Dublin, Display Interactive and Immfly, as well as AirFi – which is the dominant player in the fast growing portable W-IFE sub-segment – has grown substantially over the last five years. At the end of 2018, the five companies accounted for just 3% of the installed base. At the end of Q1 2023, this had risen to 21%.

Valour Consultancy has been analysing the IFEC market for more than a decade and our quarterly trackers provide an unparalleled deep dive into installation activity and emerging trends. This includes a tail by tail view into the exact combination of IFE system type installed across different cabin classes in the commercial aviation fleet. To find out more, or arrange a no-obligation demo of our dataset, please reach out and a member of the team will be happy to assist.