Valour Consultancy recently completed the third update to its fledgling smart airport tracker service, which provides clients with an unrivalled view of new technology adoption in airports. This includes a line-by-line view of biometric, self-service and automation equipment installations across various passenger touchpoints throughout the world. Since data was last released at the tail end of 2023, we have added an additional 343 contracts to the dataset. In particular, analysts focussed a lot of time and attention in making the self-bag drop (SBD) data as accurate as possible and, in this piece, we present some of our findings.

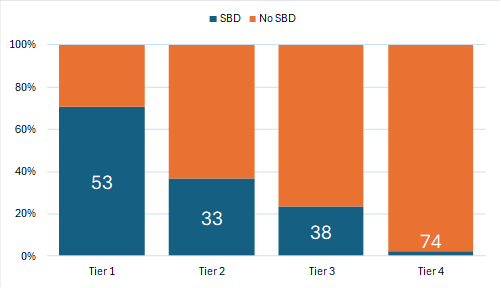

At the end of 2023, we estimate that there were just over 6,500 SBDs installed in the world’s airports. The majority (61%) can be found in tier 1 airports, which typically handle more than 30 million passengers each year. However, a sizeable portion of tier 2 (between 15 and 30 million passengers), tier 3 (5-15 million passengers) and tier 4 airports (<5 million passengers) have also deployed the technology. Overall, we have captured a total of 4,692 SBD units in our tracker (72% of the total) and by the time the next update rolls around in two months’ time, this portion of the market represented by the tracker will have further increased.

Figure 1: Proportion of Airports with SBD in Valour’s Smart Airports Tracker

Source: Valour Consultancy

Europe dominates the SBD market, comprising almost half of all installations in the tracker. Airports located in the region account for three out of the top five airports by share of SBDs deployed. Combined, airports in France (Paris-Orly and Charles de Gaulle) and the United Kingdom (London Heathrow) make up almost a quarter of the global installed base. Asia-Pacific is the next largest region – the remaining two spots in the top five are held by major tier 1 airports, Tokyo Haneda and Singapore Changi. North America has witnessed strong growth in recent years and is now firmly established as the third largest regional market. Once work on Denver International Airport’s Great Hall renovation project is completed, it will be home to one of the largest single SBD deployments in the world. As it stands, 86 of a total 176 units from Materna are installed and operational.

Just under a fifth of SBDs captured in the tracker are biometrically enabled. However, biometric adoption varies hugely by airport tier and geographic region. Some 21% of SBDs installed in tier 1 airports are biometrically enabled. This compares to 18% in tier 2, 12% in tier 3 and 5% in tier 4 airports. Biometric penetration into SBDs is highest in the Middle East at 78%. Asia-Pacific is second at 36%, followed by North America at 27%. Despite having the largest self-bag drop installed base, Europe has been very cautious when it comes to biometrics in general. Growing activity has been largely piecemeal with no widespread or coordinated efforts to build this up but the activity of airlines and groups (such as the Star Alliance Biometrics platform) is beginning to show, and the picture can be expected to change quite quickly henceforth.

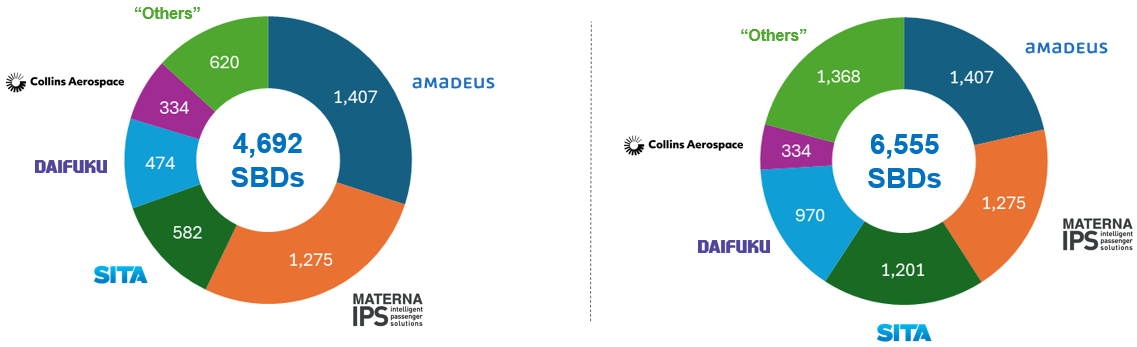

According to our data, four companies dominate the SBD market. Together, Amadeus, Materna IPS, SITA and Daifuku account for ~80% of tracked deployments. This combined share drops to about 74% when considering the SBD market in its entirety. Market shares vary hugely by region. Whilst Amadeus, for example, is strongest in Europe (and to a slightly lesser extent, in Asia-Pacific too), companies like Materna and Embross have managed to penetrate more of the North American market. SITA and Daifuku, on the other hand, derive a greater portion of their business from airports in Asia-Pacific. The latter is notable for having won several contracts in China with airports like Kunming Changshui, Chengdu Tianfu and Qingdao Jiaodong all deploying large numbers of SBDs in recent years.

Figure 2: Share of SBD Installed Base: Tracked (Left) Total Estimated Market (Right)

Source: Valour Consultancy

Valour’s smart airport tracker service runs in parallel to our comprehensive market intelligence report “The Seamless Passenger Journey in Smart Airports”. In addition to bag drop, it provides a highly granular view of where check-in kiosks, immigration kiosks, eGates (individually for pre-security, lounge access, boarding and border control), pods, totems, desk units and identity management platforms are being deployed, by whom and in what quantities. Information is gathered via a combination of primary and secondary research and alongside an Excel workbook containing all the data, clients receive a PowerPoint summary report which adds context to the numbers and provides a summary of the key headlines during the reporting period. Throughout the course of this first year, updates will be provided every two months.

If you’d like to learn more about the tracker, schedule a demo, or take a look at some samples, please don’t hesitate to contact us. Our full research portfolio is also available on request.