To supplement our in-depth annual deep dive into the in-flight connectivity (IFC) and in-flight entertainment (IFE) markets, Valour produces two tracker databases designed to keep those with a vested interest in the IFEC arena updated on installation activity and emerging trends.

Updated every quarter, these trackers present the installed base of equipped aircraft, as well as details of committed order backlogs. Data is split by key segments such as service provider, airline, geographic region and product type. And thanks to our collaboration with CH Aviation, we are also able to offer this information down to the aircraft tail level.

Last month, we released our Q1 2023 update and have put together a quick snapshot of some key findings. If you would like more information about the trackers, want to see a sample, or would like to arrange a demonstration of the data, please don’t hesitate to contact a member of the team.

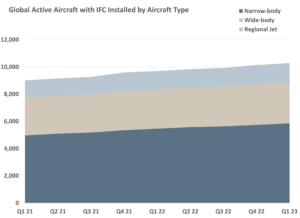

In-Flight Connectivity

- The installed base of aircraft with an active IFC solution increased for the seventh consecutive quarter, climbing to 10,278 at the end of Q1 2023.

- Viasat was the busiest service provider during the quarter, connecting 342 new aircraft.

- While Ku-band still accounts for the majority of connected aircraft at just under 5,000 tails, Ka-band equipage is growing rapidly, surpassing the 3,000 mark during the quarter.

- North America remains the largest region and, during the quarter, comprised the bulk of installations in absolute terms. However, Latin America recorded the biggest percentage change (+31%) in the installed base over the past four quarters.

- 34% of single aisle aircraft (excluding turboprops) and 67% of twin aisle aircraft can now be considered “connected”.

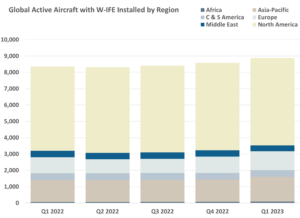

In-Flight Entertainment

- At the end of Q1 2023, there were 8,879 aircraft equipped with Wireless IFE (W-IFE). This represents a slight decrease on Q4 2022 and is mainly because Delta Air Lines stopped offering the service on aircraft without seatback screens.

- AirFi and Bluebox continue to make strong progress in this market with recent roll outs; AirFi with its deployments on easyJet and Bluebox with the roll out on the Jetstar fleet. In Q2 2022, the two companies had a combined market share of 8% but by Q1 2023, this has increased to an estimated 14%.

- Although retrofits remain the predominant source of W-IFE installations, just under 1,000 aircraft have now been fitted with the technology at the factory.

- There is still plenty of life in embedded IFE with the number of equipped aircraft continuing to grow QoQ. As of Q1 2023, 6,505 aircraft had a seatback system installed in economy class.

- Though it may be surprising to learn that there are still >3,000 aircraft with overhead IFE installed, this number continues to tick down. A 1.3% decline was recorded QoQ.

We continuously strive to make our data as accurate as we can and have implemented a number of new features in recent updates to make the trackers more user-friendly. On the back of customer feedback, we recently began offering data in a flat file format in addition to the standard deliverables. And we’ll soon be launching a new dashboard allowing subscribers to better visualise the data and highlight key trends. If you would like to learn more about any of these features, or have ideas on how we can improver further, please do reach out. And if you are an airline and want to understand the benefits of contributing to the database, we’d love to hear from you too.