Introduction

The above title is understood as the interaction between supply and demand in the maritime transport sector. Supply will lag behind capacity and demand and rates will rocket, then it will catch up, then it will oversupply and rates will fall.

This happens fairly regularly except for those spanners thrown in the works (mostly human-made spanners such as wars, pandemics, technology and regulations but nature will occasionally gum the works up too). This makes predictability onerous. There are several indices that describe the fluctuations but they are all aggregates and disguise a host of variations.

This article will discuss the details hidden in the data and the environment in which they stem from.

Freight Rate Indices

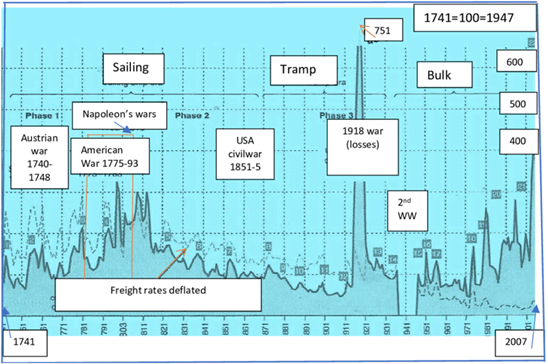

There are different types of marine cargo vessels – general cargo, dry bulk tankers (together sometimes referred to as “Tramp Shipping” because they have no fixed route or schedule), liquid bulk tankers and container vessels (sometimes referred to “Liner Shipping” as they do ply regular routes on a fixed schedule). Within these categories, there are further specialities such as reefer vessels or liquid gas carriers and different sizes of vessel. All of these have different rates. Various bodies aggregate these rates and average them out to give an overall flavour of how the maritime business is doing at any particular time. As might be expected, the historical record of these averages is roughly cyclical reflecting how the world economy is doing. Several cycles have been postulated since 1741 including a long-term cycle of roughly 60 years, a medium-term cycle of 10-20 years and a shorter-term cycle of 4-8 years. All of these have been modified by changes in technology – from wind to steam to diesel and by changes in world trading.

Figure below shows shipping freight rates across 250 years.

(1741-2007. Source: Stopford (2009), modified, p. 105; 8 war years are missing)

There are quite a few different indices each with their own audience and outlook and arriving at much different figures from each other. At first, this may seem slightly puzzling, but, if the readership is appreciated, then it begins to become clearer.

- Dry Bulk Cargo Freight Index (BDI ; Baltic Dry Index) – Capesize, Panamax, Supramax, Handysize

- Baltic Tanker Freight Index (WS ; World Scale) – Clean, Dirty (Both by route)

- Baltic LNG & LPG

- SCFI ; Shanghai Containerized Freight Index plus eleven others

- CCFI ; China Containerized Freight Index)

- Freightos Baltic Daily Index

- S&P Global Platts

- Xeneta

- Drewry

- Container Ship Freight Index (HRCI ; Howe Robinson Container Index)

The indices arising from private companies in the west are largely for investors, bankers with a nod towards ship-owners and shippers. The Chinese indices are largely aimed at users and their own internal supply chain.

There are also lots of factors to take into account and the parameters which each index sets itself. This means rates vary sometimes considerably. Despite what you may have been told size does matter so a container aboard a 24, 000 TEU behemoth travelling between Shanghai and Los Angeles will be cheaper than a container on a small coastal vessel of 2,000 TEU taking car parts from Le Havre to Newcastle, UK.

Also routes matter which is why most indices separate out voyages around the Pacific from those trans-Atlantic etc. The large container vessels, such as the one that blocked the Suez Canal recently, have restricted access for only those ports which can accommodate them which has led to congestion and delays. For example, an exporter of gooseberries from Valparaíso, Chile to Madras, India is unlikely to use a reefer container (for the adventurous, gooseberry curry, amla, with either fish or turkey is delicious) on a smaller container ship but would be dealt with fairly rapidly. However, a copper bulk cargo ship on the same route and of a much larger size can end up waiting for unloading for some time.

Freight Rate Cycles

Shipping freight cycles tread a well-worn path that have, of late, been adulterated by governmental adjustments. Once upon a time when rates were high, ship owners ordered more ships, shipyards set to work until the supply was satisfied, and then some causing rates to fall, old ships to be scrapped new ship orders to dry up until there was a shortage again and off the cycle went.

There have been at least ten “Jokers” (untoward events that cause changes to the world economy) since 1951, including the 2019 Pandemic. Governments of maritime economies are aware that an independent national shipping economy is needed including shipyards and commercial operators. They have been using the levers of government to adjust the markets to suit their aims which has interfered greatly with the cycle. At present, there is a glut of capacity that is likely to be sustained far longer than need be. In turn, this will deter investors and, in all likelihood, leave the merchant marine in a far worse state than it should be. Coupled with rising living standards and decreased enlistment in the merchant marine, a long down-turn is quite likely. Technology has shortened the short-term freight cycle to roughly six years but the overall effect of the many differing influences may well be a re-establishment of a ten-year cycle or longer.

Further articles will address freight rate forecasting and the possibility of ameliorating the excessive swings and, perhaps, measures that may be taken to forestall the twin evils of dearth and overcapacity while not constraining, too much, the healthy competitiveness of the maritime trade.