Aside from frequent discussion as to whether I’d visited Sphere, the latest striking addition to the Las Vegas skyline, a common thread ran through many of my meetings at NBAA-BACE last week: who will prevail in the hotly-contested battle for business jet connectivity supremacy? Fittingly, given its location amongst the largest concentration of gaming tables on the planet, announcements at the show and in the run-up to it give us a better understanding of where the chips may ultimately fall.

Everybody’s Talking About Starlink

We begin this article by talking about SpaceX, which kickstarted proceedings with the news that Trans-Exec Private Jets will adopt Starlink connectivity across its Gulfstream charter fleet and which also set tongues wagging with its capture of Qatar Airways the week prior. The Trans-Exec deal reportedly takes the total commitment for Starlink up to almost 500 business and commercial aviation tails and comes hot on the heels of the LEO satellite operator bagging its first fractional provider in Flexjet. Flexjet is initially introducing the solution on its Gulfstream G650s and will therefore deinstall the Viasat Ku-band equipment currently found on those aircraft.

Starlink update on the number of aircraft commited to its LEO service

Plans are afoot to certify Starlink on the remainder of Flexjet’s large cabin jets, which also includes Gulfstream G450s and Bombardier Global XRS aircraft, as well as the mid- to light jet fleet that consists of Praetor 600/500, Challenger 350/3500 and Phenom 300 aircraft. Should the deal expand in this fashion, Viasat would see its Ka-band solution being removed from the Praetor 600s too.

I say “should the deal expand” because Gulfstream took the step of issuing a maintenance and operations letter to operators following the announcement. In it, the OEM expressed concerns around the impact modifications required by the G650/G650ER STC will have on its ability to provide support and analysis of the fuselage. I’m not going to commit to a view on how this eventually plays out but will say that such a move is quite unusual. Worth mentioning though is the fact that Gulfstream has, historically, been very much aligned with the Jet ConneX (JX) solution from Inmarsat. And in the interests of balance, the OEM has said that it “will continue to work with Starlink to evaluate new technology”, and that it is “committed to validating solutions on our aircraft when and if the data supports the viability of the product”.

Regardless, SpaceX’s role as a key player in the market looks assured and, judging by the crowds at its booth, there remains considerable buzz around Starlink Aviation in the business aviation community.

OneWeb Becoming Harder to Ignore

Certain to push SpaceX every inch of the way is the newly-formed Eutelsat OneWeb. At the start of the show, the rival LEO satellite operator revealed that it had collaborated with Airbus Corporate Jets on a new IFC solution called ACJ Connect Link. Launching initially on the ACJ TwoTwenty – a VIP version of the A220 narrow-body jet – the offering will soon be made available on all Airbus ACJs, and several operators are understood to have shown an interest in becoming early adopters.

Your author on a Boeing BBJ at NBAA-BACE 2023

On the same day as the Airbus announcement, Boeing Business Jets unveiled a new way to customise cabin interiors for the BBJ 737-7, reducing costs and accelerating delivery of new VIP jets. With BBJ Select, Boeing will offer a wide range of pre-designed cabin layouts from Aloft AeroArchitects and Greenpoint Technologies. While no mention of connectivity was made in the official announcement, Valour Consultancy understands that a LEO solution will eventually be included with BBJ Select. No specific vendor has been revealed as yet but we’re evidently looking at a shootout between Starlink and OneWeb, given that the Amazon Kuiper and Telesat Lightspeed LEO constellations are still some way from commercial readiness.

Starlink and OneWeb are also set to go head-to-head in the pursuit of lighter jets. When we released last year’s report on the Future of IFC on Business Aircraft, we remarked that Textron Aviation had rejected a GEO-based satellite terminal for a line-fit position in favour of smaller form factor hardware that would operate with Starlink. Indeed, both parties confirmed as much to me during the research phase of the project. However, doing my best impression of Varys, the noted Master of Whisperers in Game of Thrones, I activated my network of little birds whilst in Vegas and they fed back that this may not, in fact, be a done deal. Indeed, it is being rumoured that the preferred solution makes use of the Hughes Network Systems’ Half-Duplex (HDX) antenna that is aimed at smaller airframes and will be used in the forthcoming Gogo Galileo solution powered by OneWeb.

That being said, it is also highly likely that, over the next 6-9 months, we’ll see a similarly sized ESA being introduced by team Musk, which will make Starlink more conducive to fitment on these same jets. So, step up to the roulette wheel and place your bets on the black of Starlink or the red of OneWeb – you’ve got as much chance of being right as I have!

GEO Remains an Important Part of the Story

Away from the chatter of LEO-based connectivity, there was plenty going on in the GEO satellite world too. Viasat announced an incentive programme for operators of legacy L-band equipment that would encourage them to upgrade to Ka-band solutions. The company also outlined an expanded range of service options that will be available across different hardware configurations from early 2024. This includes its own GAT-5510 terminal, as well as the three third-party terminals initially designed for Inmarsat’s Global Xpress (GX) constellation – the Plane Simple Ka-band solution from Satcom Direct, Orbit’s AirTRx30 and Honeywell‘s new JetWave X, which was also unveiled at the show.

Detail on what new subscription plans might look like is thin on the ground but we can likely expect some alignment with Inmarsat’s previously announced JX Evolution programme, which itself promised enhanced Ka-band speeds in excess of 130 Mbps and a raft of new service plans. A “Power by the Hour” option looks to be forthcoming too and will be offered by VAR, Satcom Direct. The move pits Viasat against Intelsat and SES which have for some time offered similarly flexible plans that allow operators to better manage operational costs according to time spent on the aircraft.

The ATG Battle Rages On

Having recently nabbed Volato as a customer and seen Davinci Jets commit to installing its technology on a large portion of its managed fleet, SmartSky Networks was rightly bullish on its prospects in the Air-to-Ground (ATG) segment. The company used NBAA-BACE 2023 to report having hit several key commercial milestones since announcing nationwide coverage of its network at the previous year’s event. This included the addition of new sales and installation partners and an expansion of the number of STCs either completed or in progress, bringing the total to 28.

And Gogo, which like SmartSky, was showcasing a business jet equipped with its ATG solution at nearby Henderson Executive Airport, was similarly optimistic about its own prospects. The main headline coming out of the show centred on Canadian fractional jet provider, AirSprint, which will upgrade its Cessna Citation CJ3+ and Embraer aircraft to Gogo 5G. The agreement also includes options for AirSprint to add the aforementioned Gogo Galileo system to its midsize jets.

Concluding Thoughts

While we’ll inevitably see further consolidation within the market, the key takeaway for me is that the business aviation fleet is clearly large enough and diverse enough to support the wide array of vendors currently vying for a slice of this lucrative pie. The large cabin segment will remain the primary battleground but huge opportunity exists in the underpenetrated mid- to light jet segments. As such, those providers of ATG solutions, as well as rival Ku- and Ka-band offerings – be they GEO- or LEO-based – can all expect to see growth if they play their cards right.

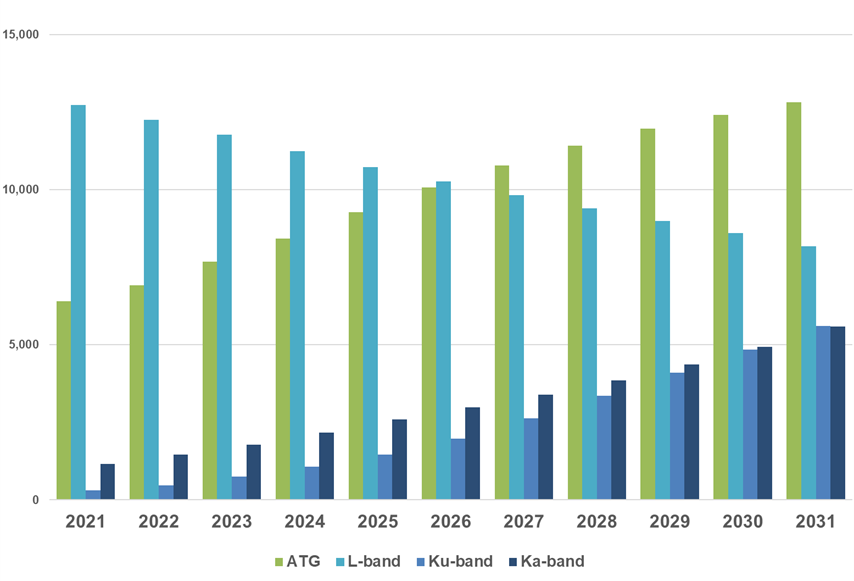

Number of IFC Terminals on VVIP and Business Aircraft by Technology Type: 2021 – 2031

Source: Valour Consultancy – “The Future of IFEC/CMS Systems on VVIP and Business Aircraft – 2022 Edition”